Where a non-member spouse transfers the amount of pension interest allocated to him or her to a retirement fund, the transfer will not be tax free, but the amount will not be taxed upon retirement.

i) Identify all the retirement funds the member belongs to – ensure the relevant funds is/are correctly identified by virtue of their employment. The court must clearly identify which funds are to be included.

ii) Establish the value of the members spouse’s pension interest. The pension interest can be no more than the (cash) resignation benefits as at the date of divorce in respect of pension and provident funds. In respect of Retirement Annuity Funds the pension interest is the aggregate of contributions plus 15.5% simple interest.

iii) Previous Divorces: Establish if any award was made to any previous divorce orders in which case such amount awarded does not form part of the pension interest available to be divided.

iv) Factors to be taken into account when deciding on the basis on which the division should take place.

The “pension interest” defined in the Divorce Act is the gross benefit. This amount may be subject to other deductions in terms of the rules of the fund.

The following should be taken into account to determine the net pension interest available:

• any existing housing loans; or

• Pension backed securities provided by the fund in terms of section 37 D

• Any maintenance orders envisaged in section 37A

A failure to take prior claims into account may result in a refusal by the fund to make payment on account of the fact that there are conflicting claims.

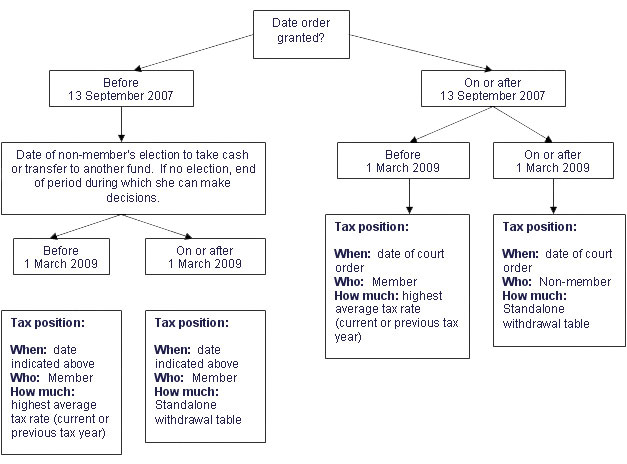

• Any tax payable on the benefit in terms of paragraph 2(a), 2(b) or 2B of the second Schedule of the income tax act. If tax is not taken into account at this stage the member will be prejudiced.

v) The divorce order: Ensure that the court in terms of section 7(8) of the Divorce Act, order the fund/s identified to make payments of a computable amount to the spouse in terms of Section 37D. Serve the order on the fund:

vi) Ensure that the fund/s receives a copy of the Section 7(8) order. The former spouse must also advise the fund if the amount allocated must be paid directly to him/her, or to be transferred to another fund.

Reference: The Manual on South African Retirement Funds and other Employee Benefits – Marx & Hanekom

(after promulgation of the Financial Services Laws General Amendment Act (Act No. 21 of 2008) and the 2008 Revenue Laws Amendment Bill)

Reference: Pension World December 2008 – Mientjie Botha

|